Compound V2: Liquidation

This article is part of the Compound V2 series. See the series index for a full list of articles.

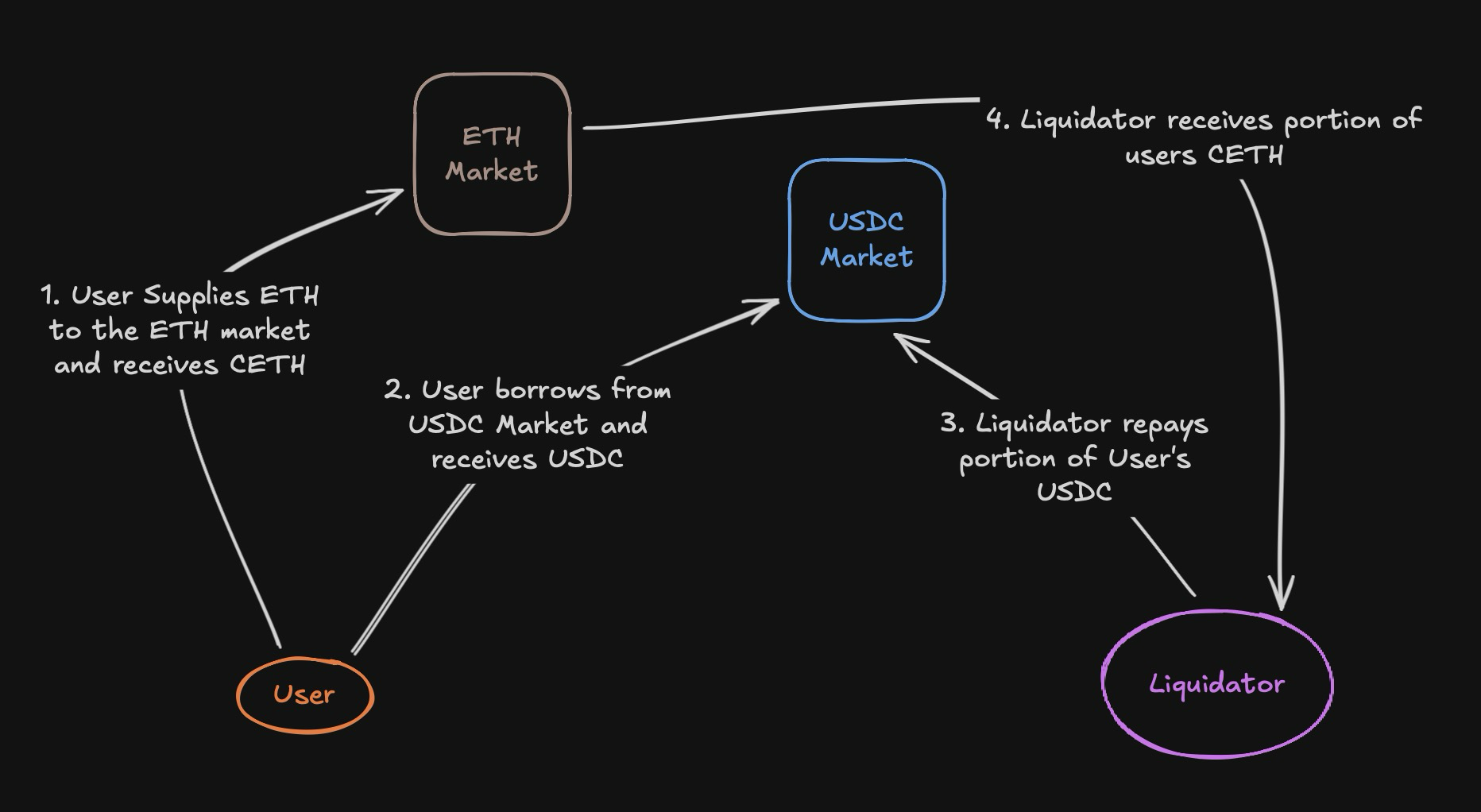

This article walks through liquidation in Compound’s cToken contract. Liquidation is how the protocol recovers bad debt: when a borrower’s position becomes insolvent, a third party called the liquidator can repay part of their debt in exchange for a discounted portion of their collateral.

Unlike minting, redeeming, borrowing, and repaying, liquidation spans two separate cToken contracts. Understanding why requires a quick recap of how Compound’s markets work.

Why Liquidation Involves Two Markets

In Compound, supplying and borrowing happen in separate markets. A user might supply ETH to the ETH market, receiving cETH as their collateral receipt, and then borrow USDC from the USDC market. These are two separate cToken contracts.

When that position becomes insolvent, the liquidator repays some of the borrower’s USDC debt in the borrow market, and in exchange seizes some of the borrower’s cETH in the collateral market. Because two contracts are involved, both need to have their interest accrued before the liquidation can proceed.

liquidateBorrowInternal

1

2

3

4

5

6

7

8

9

10

11

function liquidateBorrowInternal(address borrower, uint repayAmount, CTokenInterface cTokenCollateral) internal nonReentrant {

accrueInterest();

uint error = cTokenCollateral.accrueInterest();

if (error != NO_ERROR) {

revert LiquidateAccrueCollateralInterestFailed(error);

}

// liquidateBorrowFresh emits borrow-specific logs on errors

liquidateBorrowFresh(msg.sender, borrower, repayAmount, cTokenCollateral);

}

liquidateBorrowInternal is the entry point. It calls accrueInterest on the borrow market, then calls accrueInterest on the collateral market via an external call to cTokenCollateral. Both markets must be up to date before any calculations proceed. If the collateral market accrual fails, the liquidation reverts.

liquidateBorrowFresh

Sanity Checks

1

2

3

4

5

6

7

8

9

10

11

if (borrower == liquidator) {

revert LiquidateLiquidatorIsBorrower();

}

if (repayAmount == 0) {

revert LiquidateCloseAmountIsZero();

}

if (repayAmount == type(uint).max) {

revert LiquidateCloseAmountIsUintMax();

}

Three guards run before any state changes. The borrower cannot liquidate themselves. The repay amount cannot be zero. Unlike repayBorrowFresh, passing type(uint).max is explicitly rejected here rather than being treated as a convenience shorthand for full repayment. This is intentional: liquidators are only permitted to repay up to the close factor, a protocol parameter that caps how much of a position can be liquidated in a single transaction. Allowing type(uint).max would bypass that cap.

Repaying the Debt

1

uint actualRepayAmount = repayBorrowFresh(liquidator, borrower, repayAmount);

The liquidator repays part of the borrower’s debt by calling repayBorrowFresh directly. This is the same function covered in the repaying article. The liquidator is the payer, the borrower is the debtor, and the actual amount transferred is returned for use in the next step.

Calculating Collateral to Seize

1

2

3

4

5

6

(uint amountSeizeError, uint seizeTokens) = comptroller.liquidateCalculateSeizeTokens(

address(this),

address(cTokenCollateral),

actualRepayAmount

);

require(amountSeizeError == NO_ERROR, "LIQUIDATE_COMPTROLLER_CALCULATE_AMOUNT_SEIZE_FAILED");

The comptroller calculates how many cTokens from the collateral market the liquidator is entitled to seize. This calculation is internal to the comptroller and will be covered separately. The key point is that seizeTokens is denominated in the collateral cToken, not in underlying. The liquidator receives cTokens, not the raw collateral asset.

The amount is bounded by the close factor: there is only so much of a position that can be liquidated at once. If a borrower owes $100,000 but their position only needs $5,000 repaid to become solvent again, allowing a full liquidation would be punitive. The close factor enforces a ceiling so that liquidators can only take what is necessary to restore solvency.

Collateral Balance Check

1

require(cTokenCollateral.balanceOf(borrower) >= seizeTokens, "LIQUIDATE_SEIZE_TOO_MUCH");

A safety check to confirm the borrower actually holds enough collateral cTokens to cover the seizure.

Seizing the Collateral

1

2

3

4

5

if (address(cTokenCollateral) == address(this)) {

seizeInternal(address(this), liquidator, borrower, seizeTokens);

} else {

require(cTokenCollateral.seize(liquidator, borrower, seizeTokens) == NO_ERROR, "token seizure failed");

}

It is possible for the borrow market and the collateral market to be the same contract, for example if someone supplied and borrowed the same asset. In that case seizeInternal is called directly on the current contract to avoid making an external call back into itself. In the more common case where they are different contracts, seize is called on the collateral market, which in turn calls seizeInternal.

seize and seizeInternal

seize is the external entry point called by the borrow market on the collateral market contract. It simply delegates to seizeInternal, passing msg.sender as the seizerToken. Using msg.sender rather than a parameter is critical: it prevents a malicious caller from claiming to be a different market and seizing collateral they are not entitled to.

1

2

3

4

function seize(address liquidator, address borrower, uint seizeTokens) override external nonReentrant returns (uint) {

seizeInternal(msg.sender, liquidator, borrower, seizeTokens);

return NO_ERROR;

}

Protocol Fee Calculation

1

2

3

4

5

uint protocolSeizeTokens = mul_(seizeTokens, Exp({mantissa: protocolSeizeShareMantissa}));

uint liquidatorSeizeTokens = seizeTokens - protocolSeizeTokens;

Exp memory exchangeRate = Exp({mantissa: exchangeRateStoredInternal()});

uint protocolSeizeAmount = mul_ScalarTruncate(exchangeRate, protocolSeizeTokens);

uint totalReservesNew = totalReserves + protocolSeizeAmount;

The liquidator does not receive 100% of the seized collateral. A small portion goes to the protocol reserves, governed by protocolSeizeShareMantissa. The total seized cTokens are split: protocolSeizeTokens go to reserves and liquidatorSeizeTokens go to the liquidator.

The protocol’s share is then converted from cTokens to underlying using the exchange rate, so that totalReserves can be updated in underlying terms. totalReserves is denominated in underlying, not in cTokens.

Updating State

1

2

3

4

totalReserves = totalReservesNew;

totalSupply = totalSupply - protocolSeizeTokens;

accountTokens[borrower] = accountTokens[borrower] - seizeTokens;

accountTokens[liquidator] = accountTokens[liquidator] + liquidatorSeizeTokens;

Four state variables are updated. totalReserves increases by the protocol’s share in underlying terms. totalSupply decreases by protocolSeizeTokens because those cTokens are effectively burned: they are converted into underlying and added to reserves rather than transferred to anyone. The borrower’s cToken balance decreases by the full seizeTokens. The liquidator’s cToken balance increases by liquidatorSeizeTokens, their share after the protocol fee.

Conclusion

Liquidation is the most complex operation in this series because it crosses two markets and involves four distinct parties: the borrower, the liquidator, the borrow market, and the collateral market. The flow is:

- Accrue interest on both markets

- Verify the liquidation is permitted and within bounds

- The liquidator repays part of the borrower’s debt via

repayBorrowFresh - The comptroller calculates how many collateral

cTokensthat entitles the liquidator to - Those

cTokensare seized from the borrower, with a portion going to protocol reserves and the rest to the liquidator

The seized collateral is always in cToken form, not underlying. The liquidator receives cTokens that they can later redeem.

Compound V2 series